Start here

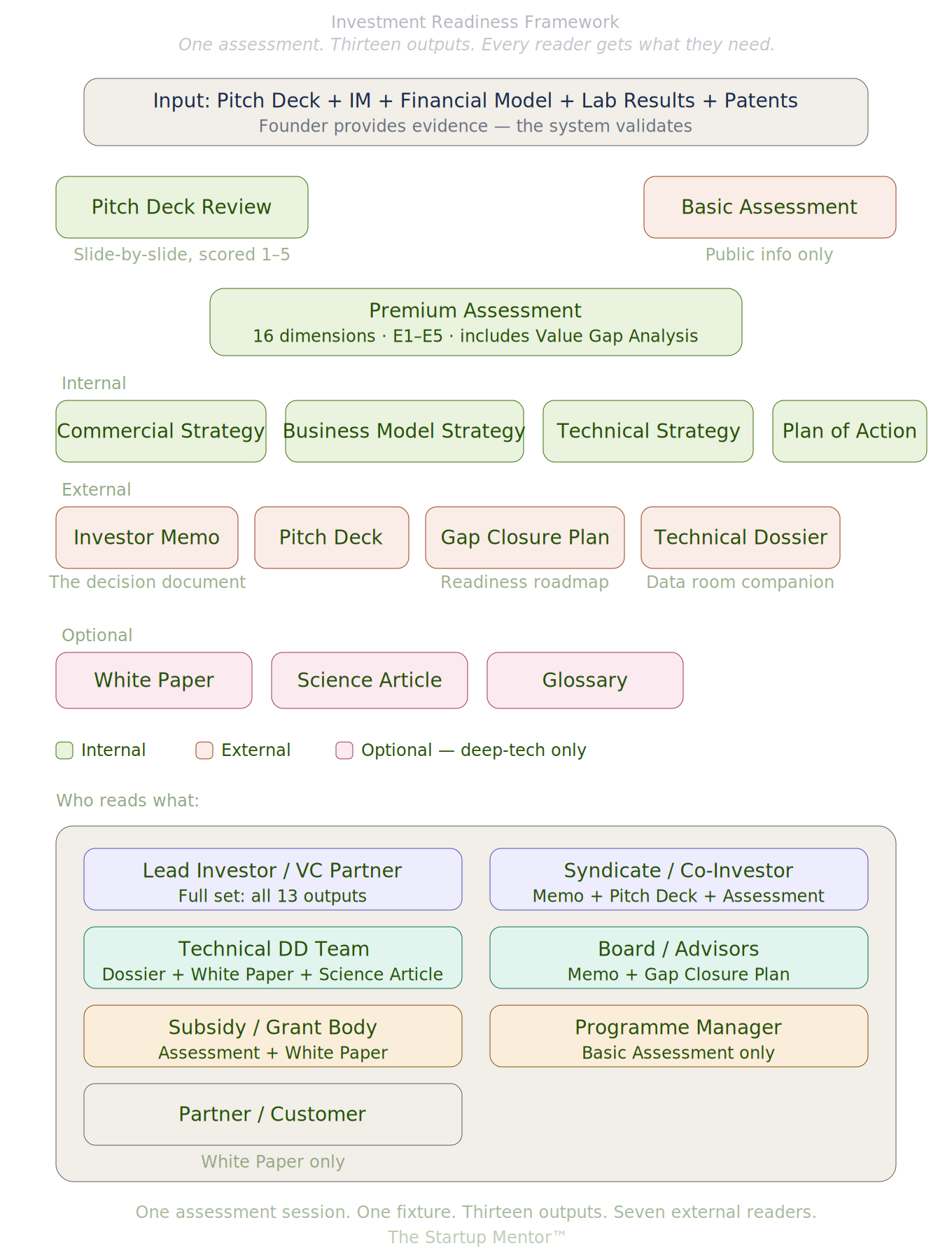

Download examplesTwo assessment depths. Both use the same sixteen dimensions, the same evidence grading, the same readiness gates. The difference is what goes in.

Basic Assessment

"What can you learn from public information alone?"

The same sixteen dimensions, the same scoring framework — built entirely from publicly available sources. Shows what the market can already see, and makes the case for going deeper. No confidential data required.

Premium Assessment

"What is actually true about this company?"

The foundation. Sixteen dimensions scored on a five-level evidence scale (E1–E5), with a Value Growth Map showing exactly where the company is strong and where value is constrained. Includes the Value Gap Analysis — every gap identified, every closing action mapped, every valuation impact estimated. Every claim traced to a source.

How to Read an Assessment

"What do all these numbers, levels, and gates actually mean?"

A 17-page guide explaining every section: pillar scores, evidence levels, the Score × Evidence matrix, readiness gates, the valuation range, and how to draw conclusions. Separate chapters for founders, investors, and programme managers.

The Investment Readiness Framework

One assessment · Thirteen outputs · Seven readersNo single document can serve every reader in the investment process. The lead investor needs the full analytical picture. The syndicate member needs the decision summary. The technical DD team needs the science. The board needs the roadmap. And the founder needs a mirror — not a sales tool, but a clear-eyed assessment of where the hidden value is and what's constraining it.

Six outputs are internal — for the company to use as a strategic compass. Seven are external — for investors, advisors, and partners. The split matters: what the founder needs to hear is not the same as what the investor needs to read.

One assessment session. One structured fixture. Thirteen outputs. Seven external readers. Each gets exactly what they need for their decision.

Internal — for the company

Strategic compassThe strategies are internal because they contain the founder's options before a decision is made. Showing an investor three possible business models signals indecision. Showing them one chosen model with evidence for why it was chosen signals clarity. The internal documents are where the thinking happens.

Pitch Deck Review

Slide-by-slide evaluation, each scored 1–5 and mapped to the framework question it should answer. Not "this slide looks nice" — "this slide is supposed to prove Need-to-Have, and it doesn't."

Commercial Strategy

The go-to-market plan. Which customers, which channels, which sequence. For a deep-tech company where the temptation is to sell to everyone simultaneously, this forces the question: who is the first paying customer and how do you reach them?

Business Model Strategy

Revenue architecture. For deep tech this is often the decision that determines everything downstream — licensing vs own-and-operate vs hybrid is a 4× difference in capital requirement and a completely different investor profile.

Technical Strategy

Technology roadmap, IP position, and the gap between lab-proven and commercially validated. Maps the scale-up pathway with risk at each transition.

Plan of Action

Prioritised next steps. What to do first, second, third — and why in that order. Not a wish list. A sequence derived from the assessment: close the weakest gate first, because that's the one that kills the deal.

External — for investors and partners

Decision documentsThe external documents are where the conclusions land. Each reader gets a tailored subset — nobody wades through material meant for someone else.

Investor Memo

The decision document. Valuation range with seven methods, investment readiness per funding round, twenty investor Q&As, and a full value growth analysis. Independently produced — that carries more weight than a company-authored IM.

Pitch Deck

Not a review — the deck itself. Generated from assessment data so every slide maps to a scored dimension. The story the founder tells, structured by the evidence the system found.

Gap Closure Plan

The readiness roadmap. Works backward from a target investment date and maps every evidence gap that must close before the round can proceed. An investor doesn't need to see that all gaps are closed — they need to see that you know which gaps exist and have a concrete plan to close them.

Technical Dossier

The data room companion. Full technical detail: process chemistry, patents with individual claims, development timeline, competitive landscape with capacity data, regulatory position, and IP economics. The document a technical DD team opens after the Investor Memo convinced them to look further.

Optional — deep tech only

Science & referenceWhite Paper

Standalone technology and market overview for anyone who needs to form a view in 30 minutes. Freely distributable — conferences, partner conversations, subsidy applications.

Science Article

Independent technical review of the scientific foundations. Written so a non-specialist investor can follow it but a domain expert finds it rigorous.

Glossary

Reference document so everyone in the process uses the same terms the same way. Small document. Disproportionate impact on communication clarity.

Who reads what

Seven readersThe founder reads everything — these are their documents. External readers each get a tailored subset:

The lead investor gets the full set. The syndicate member gets the memo, pitch deck, and premium assessment. The technical DD team gets the dossier, white paper, science article, and glossary. The board and advisors get the memo and the gap closure plan. A subsidy or grant body gets the assessment and white paper. A programme manager gets the basic assessment — no confidential data exposed. A potential partner gets the white paper only.

Seven readers. Each gets the outputs relevant to their decision. Nobody wades through material meant for someone else.

The Urban Forests example

Deep tech · ClimateUrban Forests B.V. — Passive carbon capture on building surfaces

Urban Forests is a fictional deep-tech climate company. Lab-proven chemistry, three conditional offtake agreements, a €8M Series A, a regulatory tailwind from CSRD and CBAM. It also has an unresolved business model decision, an environmental impact assessment that hasn't been started, and a production scale-up from grams to tonnes that hasn't been attempted.

The downloadable documents above were all generated from a single assessment. For a SaaS company with recurring revenue, a pitch deck might be enough to get a first meeting. For deep tech — where the science is unproven at scale, the regulatory path is uncertain, and the revenue is years away — the pitch deck is the beginning of the conversation. These thirteen outputs are the conversation itself.

Download the Basic Assessment → Download the Premium Assessment →

One source of truth. All thirteen outputs are generated from the same underlying assessment data. Update a pillar score, change a valuation assumption, add a new offtake agreement — every document regenerates consistently. No copy-paste errors. No version conflicts.

The assessment takes the materials. The documents take the assessment. The investor takes the documents. The founder never explains the same thing twice.